Why Financial Stress Is a Workplace Wellbeing Issue

Three rate rises in five months have pushed money worries to the top of the workforce health agenda. Employ Health CEO Matthew Stewart speaks with mortgage broker Jacob Decru about what employers — and employees — can actually do about it.

May 28, 2026

Share this Article:

At Employ Health, we spend most of our days inside Australian workplaces — on factory floors, in distribution centres, in offices and on construction sites. We see what the data already tells us: the health of a workforce is far more than what shows up on a manual handling assessment or a physio report. It is physical, mental, social and, increasingly, financial.

That last one is the one quietly reshaping the wellbeing conversation in 2026. Three RBA rate rises since February have added almost $3,400 a year to the average $600,000 mortgage, and the financial pressure isn’t staying neatly inside the household. It’s walking through the gates of your worksite every Monday morning.

The Data is Hard to Ignore

Recent industry research paints a confronting picture of how money worries are showing up at work. AMP’s Financial Wellness research has consistently found that roughly one in two Australian workers report some level of financial stress, with stressed employees losing close to 7.7 hours of productive time each week — a hit that adds up to a conservatively estimated $30 billion-plus annual cost to Australian workplaces.

Other Australian workplace wellbeing studies tell a similar story. Among employees experiencing significant financial problems, only around 31% report good mental wellbeing — compared with roughly 76% of those with no financial concerns. Financially stressed workers are about five times more likely to be distracted by personal money matters during work hours, and on average spend close to 11 hours a month managing those issues from their desk or smoko break.

Employee Assistance Program (EAP) providers are now consistently reporting that financial stress is one of the most common presenting issues, often sitting alongside — and frequently driving — sleep difficulties, anxiety, relationship strain and somatic complaints like headaches, jaw clenching, gut issues and elevated blood pressure. In other words, what looks like a physical health problem on the surface often has a financial story underneath.

“We treat the body in front of us, but we know the stressors driving a lot of these presentations don’t start in the workplace. Financial pressure is one of the biggest, and it absolutely affects physical health — sleep, energy, focus, recovery from injury, everything.”

— Matthew Stewart, CEO, Employ Health

What This Looks Like on The Ground

Across our onsite physiotherapy and early intervention programs, the team is noticing more workers describing classic stress-related symptoms: poor sleep that slows tissue recovery, tension headaches, jaw and neck pain, and a creeping fatigue that turns small niggles into reportable injuries. When you scratch the surface in a consult, the conversation often turns to mortgage repayments, grocery bills, kids’ costs and a quiet sense of being behind.

This is exactly why a modern workplace health strategy can’t stop at lifting technique and stretch programs. Mental wellbeing programs, mental health first aid training, psychosocial risk assessments and a strong EAP relationship all matter — and so does giving people permission to acknowledge that financial pressure is a legitimate workplace health issue, not a personal failing.

A Conversation With Jacob Decru, Loan Market Connect

To better understand what employers can usefully share with their teams, Matthew Stewart spoke with Jacob Decru, Director of Loan Market Connect, about the practical side of the rate-rise environment — and what households can do right now to take some of the pressure off.

Jacob’s headline observation will not surprise anyone who has looked at their own loan statement lately:

“Australian household debt is among the highest in the world. Many homeowners are now directing 35–45% of their take-home income just to the mortgage, and once you add other debt, total servicing costs can push past 60% of take-home pay. The hardest part is that a lot of these borrowers have never had their loan reviewed since they bought the home.”

— Jacob Decru, Director, Loan Market Connect

Jacob notes that the RBA has lifted the cash rate three times in 2026 alone, moving from 3.60% to 4.35%. On a $600,000 variable mortgage, each 0.25% rise has added roughly $94 a month — meaning households are absorbing about $282 more every month, or $3,384 across the year, just to stand still.

Five practical tactics Jacob shared

During the conversation, Jacob outlined five simple steps any homeowner can take right now. None of them require a windfall, a second job or a major lifestyle change — they’re about making sure your existing loan is working as hard for you as it possibly can.

Get a current property valuation. Property values in many parts of Australia have risen since 2021–22, which means your Loan-to-Value Ratio (LVR) may have improved without you realising it. A lower LVR can unlock a sharper rate tier.

Review your interest rate. Lenders are actively competing for well-positioned borrowers in 2026. A loan that was competitive at settlement may not be competitive now.

Ask about LVR tiers. Even a small drop — for example, from just above 80% to just below it — can shift you into a better pricing band and remove Lenders Mortgage Insurance.

Maximise your offset account. Every dollar parked in an offset reduces the daily interest charged against your loan, without locking the money away.

Don’t wait for further rises. Acting now locks in any savings immediately, instead of paying additional months at the wrong rate while you think about it.

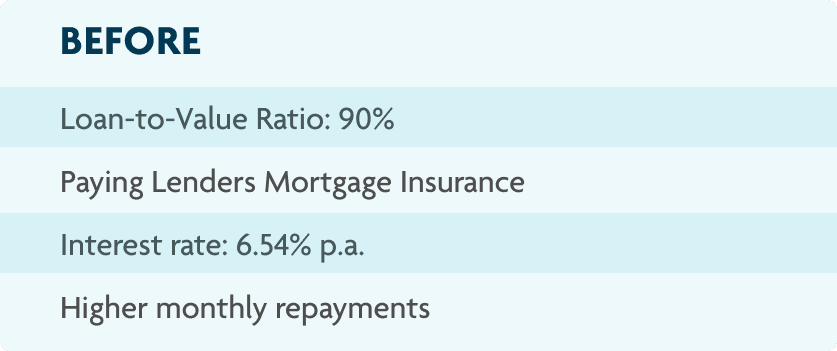

Case Study: From 90% LVR to Under 80%

Jacob shared a recent client example that illustrates how quickly the maths can change. A client purchased a home in 2021 for $900,000 with a 10% deposit, leaving them with a 90% LVR. That meant they were paying Lenders Mortgage Insurance, sitting on a higher interest rate tier because of their LVR band, and watching every rate rise compound the pressure.

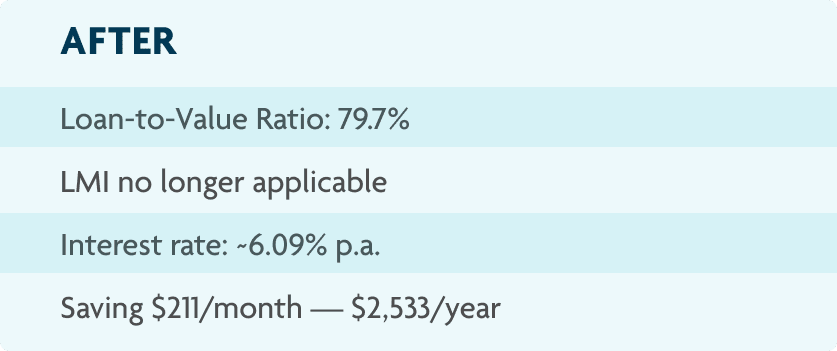

After a mortgage review, Loan Market Connect arranged a new bank valuation that lifted the property’s value from $900,000 to $1,050,000. With the loan balance now at $817,000, the LVR dropped to 79.7% — just below the critical 80% threshold. The client was refinanced to a lender using the higher valuation.

The result was a rate drop from 6.54% to approximately 6.09% p.a., a saving of $211 a month or $2,533 a year, and an end to LMI. None of the household’s income, spending or job circumstances changed. Only the structure of the loan did.

It’s a reminder that for many employees, the path to financial breathing room isn’t necessarily about earning more or spending less — it’s about reviewing the largest single line item in the household budget.

After a mortgage review, Loan Market Connect arranged a new bank valuation that lifted the property’s value from $900,000 to $1,050,000. With the loan balance now at $817,000, the LVR dropped to 79.7% — just below the critical 80% threshold. The client was refinanced to a lender using the higher valuation.

What This Means for Employers

Sharing information like this with your workforce is not financial advice, and it should never replace a licensed broker, planner or accountant. But pointing your people toward credible sources of help — and treating financial stress as a legitimate part of the wellbeing conversation — has real, measurable benefits for the workplace:

Fewer distractions, better focus and lower error rates on the job

Improved sleep, recovery and energy levels — which means fewer soft-tissue injuries and faster return-to-work outcomes

Stronger engagement with mental health and EAP supports, because the underlying driver is being named rather than hidden

A clearer signal to your team that you understand their lives don’t stop at the gate

Combining your existing safety and injury prevention programs with mental wellbeing initiatives, EAP access, and a culture that normalises conversations about financial pressure is, in our experience, one of the highest-leverage things a workplace can do in 2026.

Talking it Through With Employ Health

If you’d like to talk about how to broaden your workplace health strategy beyond the physical — including mental wellbeing programs, psychosocial risk assessment, early intervention physiotherapy and onsite health hubs — the Employ Health team would be glad to help.

Get in touch with us to book a conversation about proactive, holistic workplace health for your team.

This article shares general information only and is not personal financial, legal or medical advice. Figures referenced are illustrative and drawn from publicly available Australian research and the Loan Market Connect May 2026 Market Update. Always speak with a licensed mortgage broker, financial adviser or qualified health professional before acting on any information here.

Table of Contents

Read the latest articles

Data and Technology, Industry Insights

How Much Does an Onsite Physiotherapist Cost?

Wondering how much an onsite physiotherapist costs? Learn typical pricing in Australia, what influences costs,